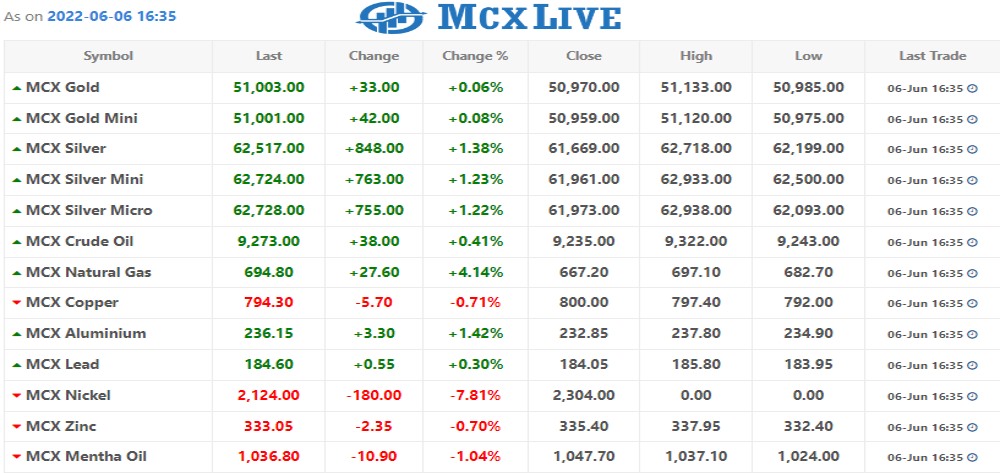

Gold prices fell on Friday, pressured by a stronger dollar and as better-than-expected U.S. jobs data raised concerns of aggressive monetary policy tightening.

Spot gold fell 1% to $1,848.67 per ounce by 1759 GMT, after earlier falling to $1,846.4. U.S. gold futures settled down 1.1% at $1,850.2.

Data showed U.S. employers hired more workers than expected in May and maintained a fairly strong pace of wage increases, signs of labor market strength.

“If the Federal Reserve sees the economy continuing to remain stable in the midst of its rate raising efforts, they might feel more emboldened to raise rates at a faster pace,” said David Meger, director of metals trading at High Ridge Futures.

Higher U.S. interest rates increase the opportunity cost of holding gold, which bears no interest, while boosting the dollar in which bullion is priced.

Cleveland Federal Reserve Bank President Loretta Mester said on Friday she was looking for “compelling” evidence that inflation has peaked, and if it hasn’t, September’s Fed meeting could see a 50 bps rate hike as well.

The dollar edged up 0.3%, while U.S. benchmark 10-year yields were close to the two-week high touched earlier in the session.

Gold prices were set to log a 0.3% dip for the week, despite the metal hitting its highest since May 9 at $1,873.79 earlier in the session.

The medium-term outlook for gold is positive, said Jigar Trivedi, a commodities analyst at Mumbai-based broker Anand Rathi Shares.

“Chinese market has reopened hence we don’t rule out retail participation and market is discounting June and July rate-hike events,” Trivedi added.

Spot silver fell 1.9% to $21.85 per ounce, down nearly 1% for the week.

Platinum was down 1.4% to $1,008.35, yet it was up 5.6% for the week, the biggest gain since Feb. 2022.

Palladium fell 3.4% to $1,983.20 and was down around 3.8% for the week.