Gold prices marked their biggest yearly decline since 2015, hemmed in by a resurgent dollar as investors prepared to usher in a new year in which the money supply could be tightened even as the threat of the Omicron coronavirus variant lingers.

Fundamentals

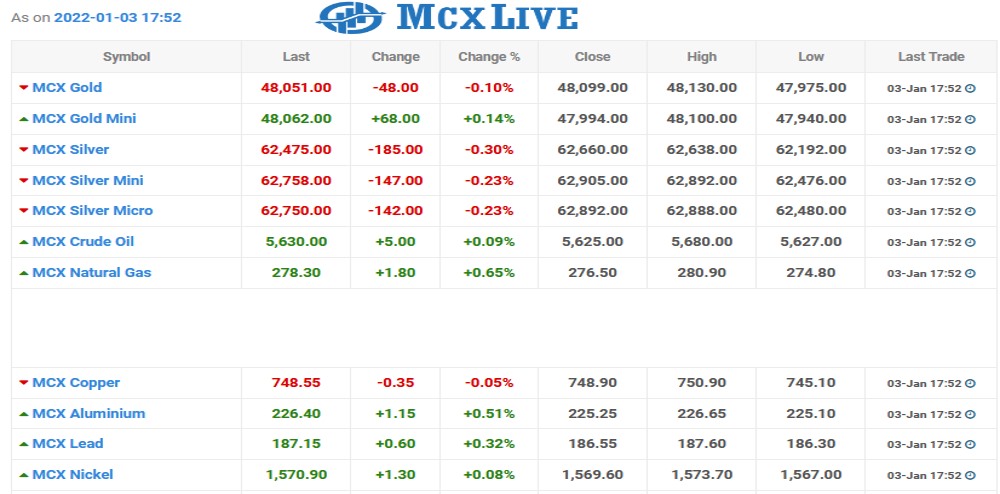

Spot gold was last up 0.4% at $1,822.11 per ounce by 11:13 a.m. EDT, after hitting a peak since Nov. 22 at $1,827.26 on Friday, helped by a retreat in the dollar and global equities.

U.S. gold futures also firmed 0.5% to $1,823.00.

Gold has eased about 4% in 2021 as a recovering global economy pushed more investors toward riskier assets and curbed interest for safe-haven assets such as bullion.

Adding to this mix were indications that central banks would speed up reining in their massive pandemic-led money printing to jump-start the economy.

Although bullion is considered a hedge against the inflation that usually results from the widespread stimulus, interest rate hikes would translate into higher opportunity cost of holding gold, which bears no interest, and lift U.S. Treasuries and the dollar.

“With U.S. 10-year yields set to hit 2% in 2022 along with transitory inflation (and of course higher interest rates), gold may be in for a downhill battle,” said DailyFX analyst Warren Venketas.

Gold posts annual decline

The Fed was expected to implement three rate hikes in 2022.

Into 2022, while concerns about the effect of the Omicron variant could support gold, higher yields might tarnish its appeal, said Han Tan, chief market analyst at Exinity.

At the same time, “gold could see several catalysts for substantial gains next year, be it a Fed policy mistake, stubbornly elevated inflation, or even a spike in geopolitical tensions.”

Spot silver rose 0.6% to $23.17 an ounce, down over 12% this year, its worst performance in seven years.

Platinum fell 0.5% to $956.50 en route to a yearly drop of more than 10%, while palladium declined 4.8% to $1,871.68, headed for its worst yearly dip in six.