Gold edged higher on Thursday, helped by a dip in the dollar as initial unemployment claim data pointed to a cooling off in the U.S. labor market, easing worries about harsher Federal Reserve rate hikes next year.

Initial claims for unemployment benefits rose 9,000 to a seasonally adjusted 225,000 for the week ended Dec. 24, the Labor Department said. Economists polled by Reuters had forecast 225,000 claims for the latest week.

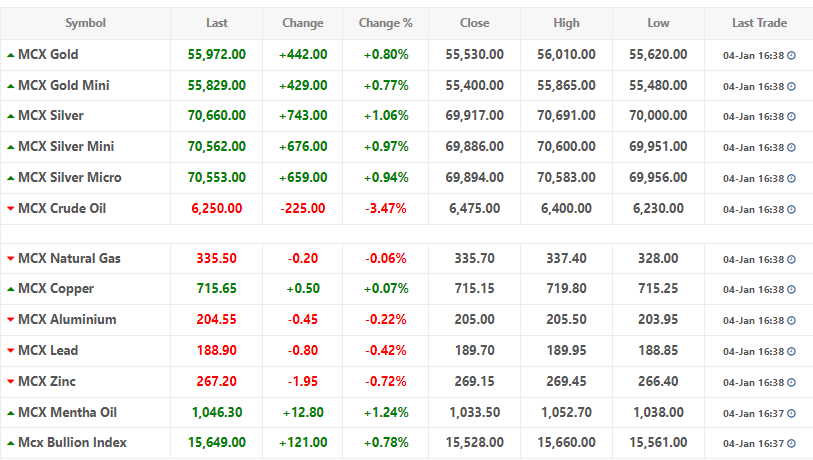

Spot gold jumped 0.7% to $1,817.30 per ounce, while U.S. gold futures settled up 0.6% at $1,826.

The jobs data led to some dollar weakness and Treasury yields backing off, causing gold to turn around, said Phillip Streible, chief market strategist at Blue Line Futures in Chicago, adding that markets were thin on volume due to the Christmas and New Year holidays.

Making gold cheaper for holders of foreign currencies, the dollar index dipped 0.6%, while benchmark U.S. 10-year Treasury yields eased after hitting a six-week high in the previous session.

Spot gold was also headed for a quarterly gain of nearly 9.5%, with prices up nearly $200 from a more than two-year low hit in September on hopes of the U.S. central bank slowing its pace of interest rate hikes.

Gold could find good support somewhere in the $1,700s, Streible highlighted, with $1,950 being a reasonable target for an average next year.

Gold earlier this week rallied to its highest in six months on China easing COVID quarantine rules further, yet doubts over official data prompted some countries to enact new travel rules on Chinese visitors.

Spot silver rose 1.8% to $23.94 per ounce.

“Encouragingly for gold bulls, silver is outperforming as this is often a good indicator of a move higher in the entire metals complex,” independent analyst Ross Norman said.

Platinum was up 4.6% to $1,054.32, while palladium rose 1.7% to $1,814.75.